The future of cryptocurrency had a rough year, to say the least.

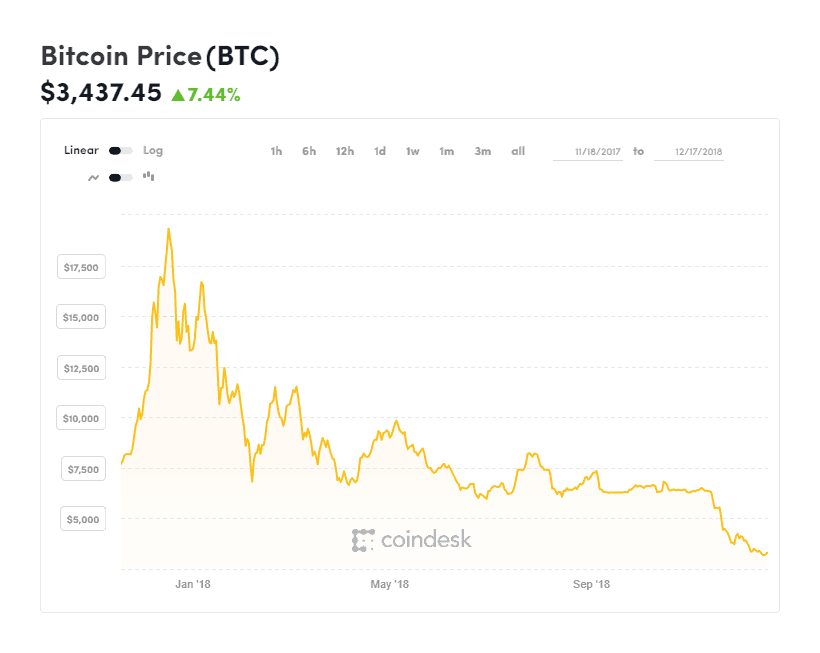

The price of bitcoin peaked at $19,783.06 on Dec. 17, 2017, exactly one year ago today.

Since then, bitcoin’s value has been in a near constant trend down, losing roughly 83 percent since that day. Currently, it is sitting at $3,437.45 an increase today of +7.44%.

The speculation of bitcoin futures being tradable on majorU.S. exchanges, military leaders in Zimbabwe overthrowing the government in part because of hyperinflation, the launch of the bitcoin futures on Dec. 11,2017, and the simple “fear of missing out” are the primary reasons for the its price jump from just over $6,000 in early Nov. 2017 to nearly $20,000 a month and a half later.

During this time, billions of dollars were invested into bitcoin and initial coin offerings (ICOs) from other digital currencies with the belief that this was the currency of the future – a digital dollar for the digital age.

But over the course of five days, the price of bitcoin plunged sharply to roughly $14,000 – losing a third of its value in less than a week due to a flurry of bad news and causing the bitcoin bubble to burst.

The initial selloff started when the Securities and ExchangeCommission (SEC) announced it was suspending trades of The Crypto Company, one of the world’s first public crypto asset and blockchain companies, until Jan. 2018 over “concerns regarding the accuracy and adequacy of information” with regards to compensation for promoting the company and possible plans for insider trading.

Coinbase, one of the leading cryptocurrency exchanges, would later announce it was also investigating insider trading and suspended bitcoin cash trading temporarily.

Then, news broke regarding

South Korea and other countries who’ve had crypto assets stolen recently blame North Korea, where research and reports found evidence the country used hackers to target individual users with “supplicated phishing attacks and malware” to steal bitcoins and other digital currencies to fund KimJong Un’s regime.

North Korea has denied having a role in any cyber attack.

Over the next three months, the bitcoin selloff would continue and fell back to the roughly $6,000 per coin price before the boom in early November 2017.

Continued reports of price manipulation at major cryptocurrency exchanges, speculation about potential regulation from the federal government, and the fear over bitcoin’s liquidity being distorted by potential institutional investors are the biggest factors leading to the selloff.

Trends for bitcoin, along with the entire cryptomarket, have continued to downward throughout most of 2018 as more people, who invested early, pulled their money to get a return on investment.

The leading concern by many investors, both in the market currently and from Wall Street, is the lack of growth in bitcoin and cryptocurrency adoption by major online retailers, both in the U.S. and around the world.

The leading U.S. online retailer Amazon, which is expected to have a 50 percent market share of the U.S. e-commerce market by the end of this year, is seen as the biggest threat or greatest hope for bitcoin and the cryptomarket – depending on your view.

While no one knows the exact reason for why Amazon won’t accept bitcoin, but some believe it’s because the volatility in the market, which is much greater than any of the government-issued currencies the online retailer currently accepts, would make it rather difficult to price items or process returns.

Amazon CEO Jeff Bezos has stayed quiet on the matter, and the company has held the position since 2014 of not accepting bitcoin because“we’re not hearing from customers that it’s right for them” and at the time, didn’t see a reason to invest in something so few people used.

However, that was when bitcoin was much less popular and since become a digital currency used by at least a million people – though that is based purely on expert estimates, since there’s no way to track the actual number of users.

The world’s largest retailer will likely have to decide on bitcoin and cryptocurrencies sooner rather than later. Whether they choose to accept it or potentially create their own digital currency using a blockchain is anyone’s guess at this point.

The clock is ticking for Amazon, because if bitcoin is truly here to stay, if other online competitors in the retail market, like eBay and Walmart, want to grab a sizeable chunk of the e-commerce market, choosing to accept cryptocurrencies before Amazon does good be a huge factor in the future of the e-commerce market going forward.

Currently, bitcoin and digital currencies, in general, are primarily seen as a tool for certain things where remaining anonymous is preferred, like with online gambling, where after purchasing, online Bitcoin casinos and Bitcoin sportsbooks allow users to convert cryptocurrencies back to the currency of their choosing – risking no money on the cryptomarket as a result.

It’s also seen as a longer-term investment by others, bought in the hopes of catching the potential second wave – one that many predict could even be bigger than a year ago – allowing them to cash in, but this “get rich quick” method would likely just trigger another collapse.

There are still many unanswered questions surrounding the relatively new currency.

More-efficient crypto mining techniques that reduce cost, transaction speed (regardless of transaction size), and energy will need to be developed to have the vision of digital currencies fully realized.

Retailers, banks, and governments around the globe have taken noticed and both have begun looking into whether to adopt and implement blockchain technology and begin issuing their own cryptocurrency.

Ultimately, the fate of bitcoin and all cryptocurrencies will fall on those three entities.

As with any currency over the course of human history, for it to be stable and worthy of trust, people need money to be safely secured, backed, and used for the purchase of all or an over

The bad news is that doesn’t seem to be

The good news is the Internet isn’t going anywhere anytime soon since it becomes ever-more important in our daily lives, and with 5G and other online advancements coming within the next year or so, the world as we know it is about to change dramatically over the next decade.

For now, at least, most of the world remains on standby, taking a wait and see approach on whether bitcoin and

As with all things: Only time will tell. Fortunately, time is on the digital currencies’ side in the digital age.

The only question that remains is: What side will we take?